During this current extraordinary time, I am having friends and family contact me and say ‘you must be really busy with all that’s happening in the markets’

I suppose by this they think that I am constantly fending off calls from clients demanding what I am doing about their reduced investment portfolio? I am proud to say that I have had very few clients ring up at all. Certainly we have kept good communication with our clients and have sent out regular communications, but these are just reminders of the basic principles which we look to deploy within our investment portfolios:

Firstly, Investment must always follow finacial planning. It is vital that goals are articulated, incorporating timescales as well as monetary amounts so that a plan can be formulated which will help those goals be achieved in the most tax efficient and lowest risk possible.

A longer term plan can afford a higher degree of volatile assets which will allow for such scenarios we are currently experiencing, to be riden out. However a shorter term plan should have a greater degree of capital preservation and therfore less exposure to volatile assets.

Secondly, there’s inherent value in markets so why not just replicate them rather than take extra risk and try to beat them?

The majority of fund managers are tasked with beating an index (In the US, most US Equity fund manangers are ‘benchmarked’ against the S&P 500) But how do they do?

This shows that of the 2,828 funds that were in existence in 2002 which were remitted to beat the S&P 500, there were only 51% of them that lasted 15 years and only 396 of them (14%) actually beat the index!

It’s no different in other asset classes with Fixed income funds fairing no better.

For a Financial adviser to pick the winners requires a crystal ball or a lot of luck.

Finally, being tactical and trying to second guess the direction of markets is more often than not an unsuccessful strategy. I love the graph below which we showed our clients in our recent communication. It is from Vanguard Investment Managers and highlights that over the last 40 years, 13 of the best 20 trading days occurred in years where markets returned negative returns and 9 of the worst 20 trading days occurred when markets returned positive returns. The chart below highlights the proximity of those days and demonstrates how close the best days are to the worst days.

We had a very recent example of that back on March 16th when the FTSE 100 (the index of the largest 100 companies in the UK) rose by an unprecedented 9.1%, a rise which no tactical wealth mananger could have predicted.

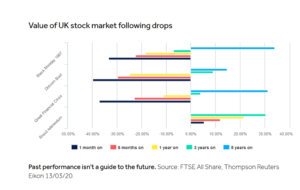

If you have a clearly defined long term financial planning goal, staying disciplined and not panicking is the best solution. In many instances, the speed of the recovery (i.e. the time it takes for markets to return to their original level before a fall) can be surprisingly short considering the depth of the fall. The graph below shows certain bear markets (most notably the credit crunch in 2008) and the level of growth achieved over different timeframes if you had invested at the top of the market before the crash. In the instance of the 2008 crash (called ‘the great financial crisis’ in this graph) within three years, an investor was back in profit.